A Journal Entry That Debits Finished Goods and Credits Work in Process Records the

What is Cost of Goods Manufactured (COGM)?

Cost of Goods Manufactured (COGM) is a term used in managerial accounting that refers to a schedule or statement that shows the total production costs Absorption Costing Absorption costing is a costing system that is used in valuing inventory. It not only includes the cost of materials and labor, but also both for a company during a specific period of time. Just like the name implies, COGM is the total cost incurred to manufacture products and transfer them into finished goods inventory for retail sale.

To learn more, launch CFI's free accounting courses!

The formula to calculate the COGM is:

Add: Direct Materials Used

Add: Direct Labor Used

Add: Manufacturing Overhead

Add: Beginning Work in Process (WIP) Inventory

Deduct: Ending Work in Process (WIP) Inventory

= COGM

Example Calculation of Cost of Goods Manufactured (COGM)

This can be more clearly seen in a T-account. For example, let's say that a company that manufactures furniture incurs the following costs:

Direct Materials: $100,000

Direct Labor: $50,000

Manufacturing Overhead: $60,000

Beginning WIP Inventory: $10,000

Ending WIP Inventory: $30,000

| Work in Process (WIP) Inventory | |

| Beginning Balance 10,000 Direct Materials 100,000 Direct Labor 50,000 Manufacturing Overhead 60,000 | 190,000* COGM |

| Ending Balance 30,000 | |

With this information, we can solve for COGM, which is on the credit side of the WIP Inventory T-Account.

COGM = 10,000 + 100,000 + 50,000 + 60,000 – 30,000 = $190,000*

To learn more, launch our free accounting courses!

Determining Direct Materials Used

In order to determine the actual direct materials used by the company for production, we must consider the Raw Materials Inventory T-account. Raw materials inventory refers to the inventory of materials that are waiting to be used in production. For example, if a company were to make a raw material purchase for use, these would be recorded in the debit side of the raw materials inventory T-Account.

In addition, if a specific number of raw materials were requisitioned to be used in production, this would be subtracted from raw materials inventory and transferred to the WIP Inventory. Raw materials inventory can include both direct and indirect materials. Beginning and ending balances must also be used to determine the amount of direct materials used. Let's also examine the following raw materials T-account.

| Raw Materials Inventory | |

| Beginning Balance a Purchases of Raw Materials b | d Raw materials used in production |

| Ending Balance c | |

The raw materials used in production (d) is then transferred to the WIP Inventory account to calculate COGM.

To learn more, launch our free accounting courses!

Determining Direct Labor and Manufacturing Overhead

Determining how much direct labor was used in dollars is usually straightforward for most companies. With time logs and time sheets, companies just take the number of hours worked multiplied by the hourly rate. For information on calculating for manufacturing overhead, refer to the Job order costing Job Order Costing Guide Job Order Costing is used to allocate costs based on a specific job order. This guide will provide the job order costing formula and how to calculate it. As an example, law firms or accounting firms use job order costing because every client is different and unique. Process-costing, on the other hand can be used guide.

Linking COGM to COGS

Once all the individual parts are calculated and used to figure out the total cost of goods manufactured for the year, this COGM value is then transferred to a final inventory account called the Finished Goods Inventory account, and used to calculate Cost of Goods Sold Accounting Our Accounting guides and resources are self-study guides to learn accounting and finance at your own pace. Browse hundreds of guides and resources. . Finished Goods Inventory, as the name suggests, contains any products, goods, or services that are fully ready to be delivered to customers in final form. The following T-account shows the Finished Goods Inventory. Beginning and ending balances must also be considered, similar to Raw materials and WIP Inventory.

| Finished Goods Inventory | |

| Beginning Balance a Cost of Goods Manufactured b | d Cost of Goods Sold |

| Ending Balance c | |

With all the pieces together, we can construct a full Schedule of Cost of Goods Manufactured and Cost of Goods Sold.

Final Cost of Goods Manufactured (COGM) Formula

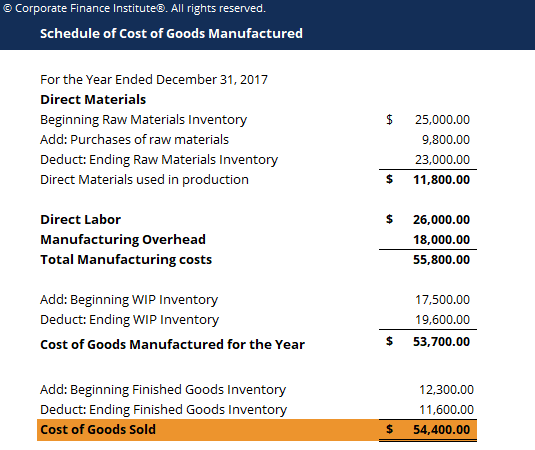

| Schedule of Cost of Goods Manufactured For the Year Ended December 31, 2017 | |

| Direct Materials Beginning Raw Materials Inventory Add: Purchases of raw materials Deduct: Ending Raw Materials Inventory Direct Materials used in production | a b c d = a + b – c |

| Direct Labor | e |

| Manufacturing Overhead | f |

| Total Manufacturing costs Add: Beginning WIP Inventory Deduct: Ending WIP Inventory Cost of Goods Manufactured for the Year Add: Beginning Finished Goods Inventory Deduct: Ending Finished Goods Inventory | g = d + e + f h i j = g + h – i k l |

| Cost of Goods Sold | m = j + k – l |

To learn more, launch our free accounting courses!

Why is COGM Important for Companies?

In general, having the schedule for Cost of Goods Manufactured is important because it gives companies and management a general idea of whether production costs are too high or too low relative to the sales they are making.

For example, if a company earned $1,000,000 in sales revenue for the year and incurred $750,000 in Cost of Goods Sold, they might want to look at ways to reduce their manufacturing costs to increase their gross margin percentage.

Comparatively, if another company earned $800,000 in sales revenue and incurred only $400,000 in COGS, even though the company's sales were lower, their gross margin percentage is much higher, which makes the latter company substantially more profitable.

Therefore, by having a general picture of what the company is incurring in terms of manufacturing costs in all its specific components of materials, labor, and overhead, management can examine these areas more thoroughly to make any necessary adjustments or changes to maximize the company's net income.

To learn more, launch our free accounting courses!

Download the Free Template

Enter your name and email in the form below and download the free template now!

Cost of Goods Manufactured Template

Download the free Excel template now to advance your finance knowledge!

Additional Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ Program Page - CBCA Get CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

- Accounting careers Accounting Public accounting firms consist of accountants whose job is serving business, individuals, governments & nonprofit by preparing financial statements, taxes

- T Accounts T Accounts Guide If you want a career in accounting, T Accounts may be your new best friend. The T Account is a visual representation of individual accounts

- Cost of Goods Sold Accounting Our Accounting guides and resources are self-study guides to learn accounting and finance at your own pace. Browse hundreds of guides and resources.

- Marginal Cost Formulas Marginal Cost Formula The marginal cost formula represents the incremental costs incurred when producing additional units of a good or service. The marginal cost

A Journal Entry That Debits Finished Goods and Credits Work in Process Records the

Source: https://corporatefinanceinstitute.com/resources/knowledge/accounting/cost-of-goods-manufactured-cogm/

{kind=link}

ارسال یک نظر for "A Journal Entry That Debits Finished Goods and Credits Work in Process Records the"